GRANT WRITING

Grant Writing Basics

Common Elements of a Grant Application

Proposal Development

Planning

Writing a Competitive Proposal

Goals and Objectives

Activities

Module Evaluation

GRANT BUDGETING

Budgeting Basics

Essential Budget Elements

Building Your Budget

Budget Management

Module Evaluation

GRANT MANAGEMENT

Management Basics

Post-Award Basics

Common Terms

Module Evaluation

R E S O U R C E S

GRANT WRITING

Grant Writing Basics

Common Elements of a Grant Application

Proposal Development

Planning

Writing a Competitive Proposal

Goals and Objectives

Activities

Module Evaluation

GRANT BUDGETING

Budgeting Basics

Essential Budget Elements

Building Your Budget

Budget Management

Module Evaluation

GRANT MANAGEMENT

Management Basics

Post-Award Basics

Common Terms

Module Evaluation

R E S O U R C E S

From “The Grant Seeker’s Guide to Winning Proposals”

(Download PDF )

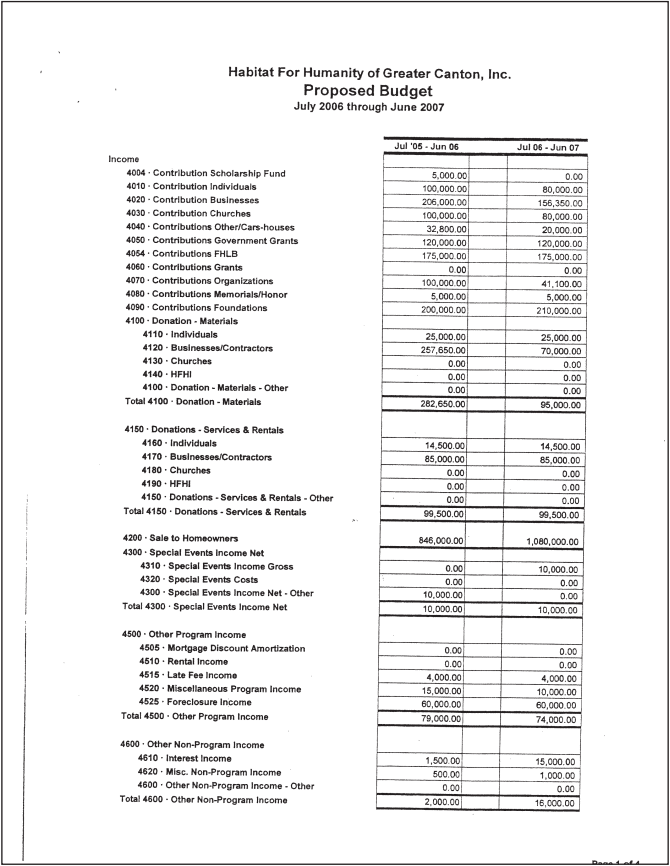

Income/revenue generally comes from these sources:

- – Grants

- – Contracts (fee for service)

- – Individual Contributions (e.g. donations)

- – Sale of Goods (e.g. selling tickets to a special event)

It is important to note that not all funders will require you to include project income in your budget proposal. Inclusion of income detail is usually required if other financial support has been committed to your project through foundation funding, in-kind (non-monetary) gifts, government sources or individual contributions.

These details become important when dealing with federal and state funding agencies as federal regulations prohibit agencies from using federal funds to supplant existing funds. Generally, supplanting occurs when a State, local, or Tribal government reduces State, local, or Tribal funds for an activity specifically because federal funds are available (or expected to be available) to fund that same activity. When supplanting is not permitted, federal funds must be used to supplement existing State, local, or Tribal funds for program activities and may not replace State, local, or Tribal funds that have been appropriated or allocated for the same purpose.

Additionally, federal funding may not replace State, local, or Tribal funding that is required by law. In those instances when a question of supplanting arises, the applicant or grantee will be required to substantiate that the reduction in non-federal resources occurred for reasons other than the receipt or expected receipt of federal funds.

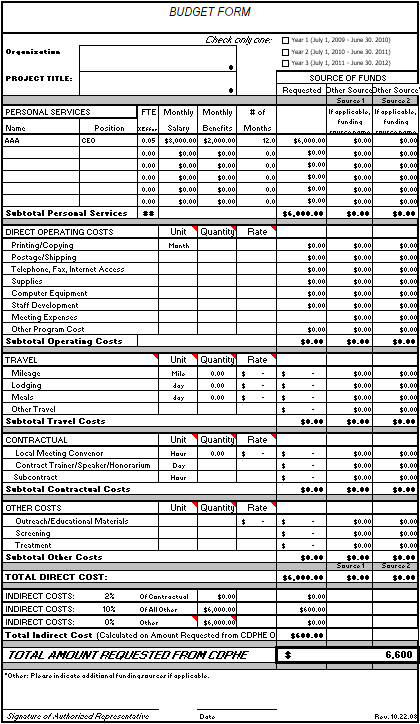

Budget Form

(Download Sheet)

Remember, the amount of funding that you are requesting should be consistent with the level of effort necessary to accomplish the goals and objectives of the project. Your budget proposal should include a list of all personnel and non-personnel expenses related to the operation of the project. These costs are broken down into two categories: Direct Costs and Indirect Costs.

Direct & Indirect Costs

- Direct Costs are those that can be identified specifically with a particular sponsored project. These costs are variable and include, but are not limited to: salaries, fringe benefits, supplies, equipment, operating costs, patient costs, research costs and travel.

- Indirect Costs, sometimes called Facilities and Administrative Costs (F&A), or Overhead, are those that support the entire organization or are incurred for common or joint objectives that cannot be easily identified with a specific sponsored project. These include, but are not limited to: costs of administrative personnel, rent, building maintenance, most utilities, general office expenses, and general administrative costs.

Calculating Indirect Cost Rates

Large organizations that routinely receive federal grants will have an established “federally negotiated indirect rate” that they are permitted to use when applying for federal or state funding. Organizations that do not have a federally negotiated rate will need to calculate these costs on their own. The formula used for allocating indirect costs to project budgets is usually based on the organization’s overhead costs to the organization’s total program expenses.

Example: For most institutions the negotiated F&A rate will use a modified total direct cost (MTDC) base, which excludes items such as: equipment, student tuition, research patient care costs, rent, and sub-recipient charges (after the first $25,000).

Sample Budget Detail Worksheet (Download Worksheet)

The proposal’s budget section has two components: the budget and the budget justification. Most funders require applicants to justify the need and explain the rationale for each requested budget line item. In other words, the budget presents each line item; the budget justification explains why each item is necessary for the project and how the requested amount was calculated.

Budget justifications should typically follow the same format as the budget categories and line items presented in the budget worksheet. However, you should read the application instructions carefully to identify which items must be justified and what information to include.

Generally, the following items require a written justification:

- – Personnel (who, effort)

- – Fringe benefits (list rates used)

- – Supplies

- – Travel (destinations, duration)

- – Equipment and quotes, if available

- – Subcontracts (in the same format as prime)

- – Other costs associated with the project (service center costs, publications, etc., if allowed)